Super funds for super professionals

Harrison Lane

9.5% of your salary that most of us don’t even think about!

Generally speaking, if you’re 18 years old or over, and you earn $450 or more in a month (pre-tax), then your employer is obligated to pay 9.5% of your salary into your superannuation fund – how good is that! And better yet – pending any legislation changes – this amount is likely to increase incrementally to 12% by 2025.

But managing your super, let alone choosing a super fund can be overwhelming. Which fund has the best returns? How much should I be paying in fees? Superannuation can be confusing.

But never fear, we’re here to break it down. In this email we’ll dive into the following questions:

- Which super fund should I choose?

- What is the right investment option for me?

- How can I avoid some common yet costly mistakes?

If I can’t spend it now, why should I think about it?

Your superannuation is a retirement nest egg. You contribute a small portion of your income so that by the time you retire there is a sizeable investment to spend on whatever you want, from your grandkids’ education to sailing around the Bahamas.

But it ain’t that simple. Working in the superannuation industry for multiple years, I quickly realised that many super funds are not up to scratch, either due to huge fees or poor investment expertise. It’s no wonder performance between super funds varies so much!

And even then, the right super fund (and investment option) can differ between people. Choosing the right super fund for you and understanding the risk involved is key to a successful pot of gold at the end of the working rainbow. Yet despite its importance, it’s amazing how little we actually look at our super. What am I invested in? Is it too risky? Is it not risky enough? Am I getting the best bang-for-buck?

Below we highlight our top tips to ensure your super fund is working as hard as you (or maybe even harder!).

Alright Houston, what’s the solution?

Which super fund should I choose?

With around 200 superannuation funds in Australia (although this number is falling as the industry consolidates), it can be a daunting task to select one that’s most right for you. As a result, many people default to the superannuation fund selected by their employer. While this can be a reasonable option, it’s important to know what’s out there to make the best decision possible.

There are many factors which go into our list of recommended super funds. We’ve broken down our top picks into these recurring categories:

Price is Right

Our top picks in the “Price is Right” category focus primarily on strong expected returns and low fees.

- Strong expected returns: A super fund will either invest your money directly or invest it with fund managers (funds specifically dedicated to investing money), who will invest it on your behalf. Super funds, therefore, need to be able to select fund managers and manage the overall portfolio as efficiently as possible. Skill in super funds is tough to measure, and despite what many people think, past performance won’t determine how a fund will perform in the future! Organisational governance, investment expertise and ability to research fund managers are all important factors.

- Low fees: Fees play a big part in our assessment because while skill might be hard to determine, fees are certain and can greatly influence your overall return. Super funds will charge administration and investment fees, and these can vary dramatically between super funds. Typically, large super funds – in particular industry super funds (which are not-for-profit) – have lower fees. They can also afford to pay for large, skilled investment teams, and so we tend to be biassed towards them.

- Assets under management measured as at 30 June 2019

- MySuper (default) Balanced Option

- Returns (net of fees) to 30 June 2019

- Investment fees from 1 July 2018 to 30 June 2019; investment fees vary from year to year and are expressed as a percentage of your account balance

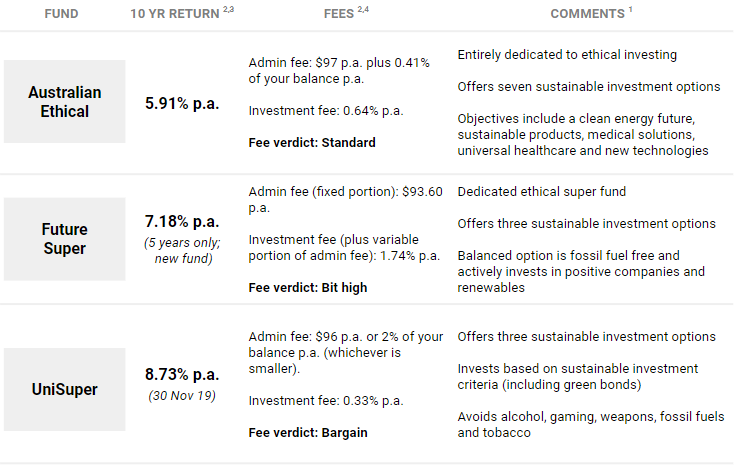

More than Money

If you’re looking for a more ethical approach to your super, our top picks in the “More than Money” category incorporate sustainable investing options.

Incorporating sustainability into a super fund’s major investment options is increasingly common, taking into consideration environmental, social and governance factors. Many funds, however, offer a dedicated ethical investment option, combining positive screens (investing in “good” things) and negative screens (excluding “bad” things).

Sustainable investing can vary between super funds, and include things such as excluding tobacco, controversial weapons and investments in fossil fuels and carbon-intensive businesses. These investment options go the extra yard when it comes to sustainable investment.

- Default balanced sustainable investment option

- Returns (net of fees) to 30 June 2019, unless otherwise stated.

- Investment fees from 1 July 2018 to 30 June 2019; investment fees vary from year to year and are expressed as a percentage of your account balance

What is the right investment option for me?

Most super funds have several investment options based on different levels of risk and return. Generally speaking, you’ve gotta risk it for the biscuit! A high return-seeking option will be riskier, investing in more volatile assets such as equities and opportunistic property, infrastructure and private equity. A low return-seeking option will be less risky, investing a greater proportion of your portfolio into more predictable things such as bonds and less risky property.

Everyone’s risk tolerance is different and can depend on your financial situation outside of super. If you’ve just started working we would typically recommend a higher return-seeking option. This is because you have a longer investment time frame, and even if there are some periods of poor performance, overall you should expect a higher return in the long run.

How can I avoid some common yet costly mistakes?

The most common issue with people’s super is having multiple accounts with different super funds. Why is this a problem? More accounts equals more fees. This is fun for the super funds, but not you.

Millions of Australians fall victim to this, which collectively costs billions in additional fees each year. Luckily, MyGov allows everyone to see which super funds are attached to their name, and easily consolidate funds into a single account (see this ATO webpage for more details).

So, if you’re not sure where the super is from your first job in retail / fast food / telemarketing, check it out and make sure you’re not paying unnecessary fees!

Let’s wrap this up

And there we have it – some top tips to make sure your superannuation is hard at work!

Before we sign off, one final tip: try to stay up to date with your super! Most super funds will send regular communications, and many of our top picks have great websites and mobile apps to help you understand what you’re investing in, and how it’s performing. We recommend setting yourself a reminder every three months to log into your account and see how it’s going. It’s likely to help with your other investments too!

Stay tuned for upcoming topics or check out or other useful articles here. We’ve got plenty more gold to help you make the leap from top student to top professional!

Got feedback? We’d love to hear from you! Shoot us an email at [email protected]

Who’s behind the scenes

Not signed up to The Launchpad yet?

Subscribe below to get the full experience!

|

|

|